A Call to Action

There is a major problem with how Canadian group Dependent Life insurance contracts define eligible children, and it is time to come together as industry stakeholders to ensure we properly take care of young families.

It’s time to bring outdated legacy definitions up to modern standards, and to ensure that no one in the Canadian insurance industry going forward should ever need verify the number of hours or days lived to determine if an infant death qualifies for coverage under a Dependent Life benefit. We can do better.

CGIB Member Gavin Mosley has made it his mission to help rectify this problem.

I'm asking for your support...

1. Sign the petition

2. Share it with your clients and their employees (if willing)

3. Share as widely as you can (friends, family and the rest).

For more details, read here. https://www.change.org/p/modernizing-group-dependent-life-insurance-coverage-for-children

Initial "INFORMAL" TPA/ Insurer feedback

Beneva:

Benefits by Design:

Co-operators:

Co-operators supports this initiative and is deeply committed to building resiliency and serving the unmet needs of Canadians and the communities we live. As such, our dependent term life wording is aligned to reflect that.

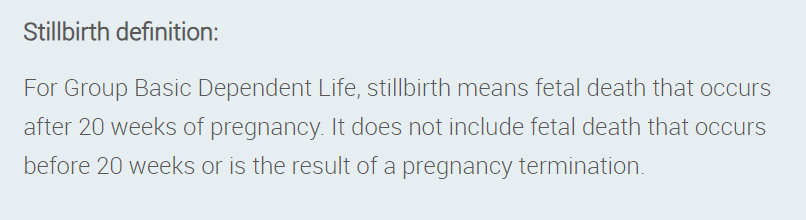

Our standard dependent life wording includes a pre-natal benefit starting at 20 weeks gestation to help provide financial assistance to the plan member in the event of an eligible dependent’s death. This benefit is payable to the plan member once the gestational period has reached 20 weeks or more, to a maximum not exceeding the Dependent Life insurance amount for a dependent child in the event of stillbirth.

We still offer options for large groups to start coverage upon live birth, however our standard is starting at 20 weeks gestation.

Clear Benefits:

I agree this is important. ClearBenefits.ca addressed the Dependent Life issue in 2007 and took the position to include a compassionate pre-natal definition of eligibility.

Canada Life:

Desjardins:

Our standard at Desjardins for Perform Plus, as of April 3rd dependent life ( from 20 weeks gestation) is our standard.

However, sponsors do have the choice to still have the live birth definition ( we have removed the option of 24 hours after birth). We would amend the contract to the new definition if requested (at no change in rates).

In large group our standard is also the same however the sponsor still has the options of live birth, 24 hours and other (to match different definitions for large cases).

Empire Life:

We fully agree and support this initiative. We updated the language in our contracts over 5 years ago

Still Born: death claims for stillborn babies are still reviewed on a case by case basis as any claim is. However, the guidelines are, if any official documents can be produced ie, Death Certificate and/or a statement from a Funeral Home we will consider the claim eligible as a dependent. The baby does not have to be alive at birth, the baby does not even need to take a single breath. As long as we can retrieve these documents, a still born will be eligible.

(Our contracts don't actually specify this language for dependant children to allow for greater flexibility and as mentioned still birth is also considered on a case by case basis.)

Equitable:

|

IA:

Manulife:

Medavie Blue Cross:

Pacific Blue Cross:

I wanted to say thank you for addressing this challenging life situation that many Canadian families endure. Coping with early infant loss or experiencing a stillbirth is an extremely personal and difficult time, and benefits should provide individuals and families with the support they need during this time. Updating our industry standard to include appropriate coverage during this phase of life is the right thing to do.

While Pacific Blue Cross does provide Dependent Life coverage from the time of live birth, and we have added a “New Parent Boost” into many of our individual plans that offers increased mental health and physiotherapy coverage to support new parents during pregnancy and post-partum, there is still more we can do. We’re looking at the opportunity to update our Dependent Life coverage to begin from 28 weeks gestation, to ensure fair and equitable levels of protection to all our members.

RBC:

Just wanted to let you know that your recent posts about Dependent Life coverage not always starting at live birth put me on a mission at RBC! Although “from live birth” has been our standard for quite some time, we ran reporting nationally and found many policies that had old policy language of either 24 hours or 14 days.

The RBC Insurance account reps across the country are now addressing each of these policies with our brokers in order to recommend the change to “from live birth”. I was happy to see that I had none in my region that needed correction.

Anyway, just wanted to thank you for the nudge, it has been a great pro-active initiative that will benefit many of our clients!

Sun Life:

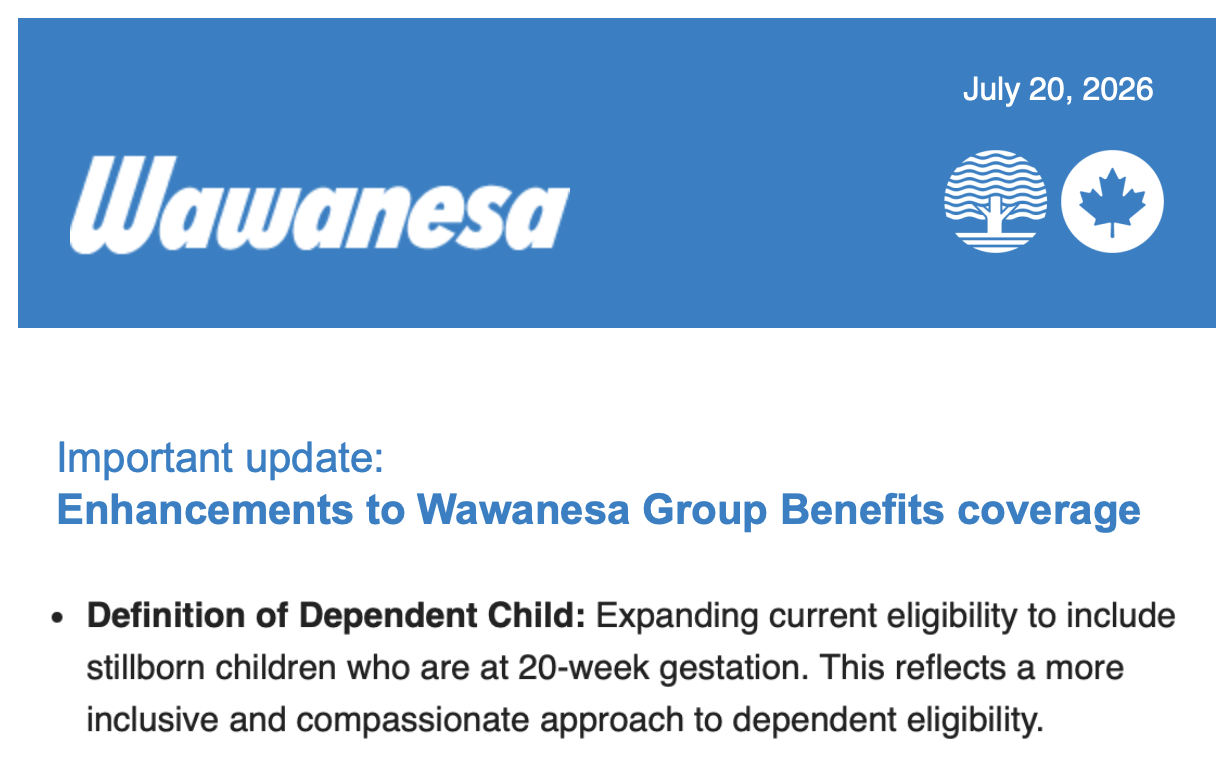

Wawanesa:

GAVINS CALL TO ACTION TO THE CLHIA

My name is Gavin Mosley, and I am a 20 year group benefits insurance industry veteran writing to you regarding an important group benefits insurance industry issue that aligns closely with CLHIA’s mission to serve its members in areas of common interest, need or concern.

A Call to ActionThere is a major problem with how Canadian group Dependent Life insurance contracts define eligible children, and we are asking CLHIA to create a new guideline to ensure the group benefits industry maintains trust with clients while taking better care of young families when they need it most.

We wish to bring outdated legacy definitions up to modern standards, and to ensure that no one in the Canadian insurance industry going forward should ever need to verify the number of hours or days lived to determine if an infant death qualifies for coverage under a Dependent Life benefit. We can do better.

Background

The problem was brought to the forefront for me when a client named Sandy phoned looking for bereavement support, as her twin grandsons had tragically passed away at birth. Although the pregnancy was deemed high risk due to the twins sharing the same placenta, their parents, Sara and Zach, were optimistic as they progressed closer to their due date. Unfortunately, Sara went into early labour and the hospital confirmed a rare pregnancy condition causing severe complications. The doctors found one twin having a very faint heartbeat and the other going into kidney failure, and soon after delivery, their sons sadly passed away - Nolan within the first day and Patrick the second day.

After hearing this heartbreaking account, I asked if the parents had group insurance at their respective employers, which was the case. It was at this point where my heart sunk deep into my chest, where I directed them to check if there was a Dependent Life Insurance benefit on the plans, but also to check if the definition of an insurable child was “from live birth”, “after 24 hours” or “after 14 days”. I was concerned there was a chance an insurer might give this family more bad news if their policy was anything but “from live birth”. It ended up that the parents had not known about there being Dependent Life coverage, and thankfully they found that both plans included a “from live birth” definition which means that benefits were payable.

The proceeds were set aside to help with final expenses and to create an education fund for a potential future sibling. In 2022, Sara and Zach were blessed to welcome their daughter, Julia, whose education will be funded in part by her older brothers (and indirectly because their plans were set up according to modern standards by their employers and their benefits advisors).

Although these policies in particular paid out, this story could have had very different outcomes:

o What if the twins were stillborn, or if the employers wanted to save a few cents on their Dependent Life rate and opted for a 14 day benefit, and both claims were declined?

o What if their employers chose a carrier with a benefit that started after 24 hours, where Patrick’s claim would be approved and Nolan’s declined by a matter of hours?

o Apart from their twins, Zach and Sara also unfortunately suffered loss through miscarriages, which were not covered.

Industry PetitionTo determine whether this issue was of common concern, we set up a petition that was signed by 10,042 industry stakeholders spanning individuals working at insurance companies and brokerages who do not want to be in a position of having to sell or service a 14 day child definition, as well as plan sponsors and plan members who unanimously agreed they do not want to be covered for a 14 day child definition. The petition can be found here:https://www.change.org/p/modernizing-group-dependent-life-insurance-coverage-for-children.

A Call to Action

Anyone working in the Canadian group insurance industry should never be put in a position of having to verify the number of hours or days lived to determine if an infant death qualifies for coverage under a Dependent Life benefit. The price difference is immaterial from an actuarial perspective, and the majority of insurers and underwriters already quote a “from live birth” definition as standard. There are, however, a number of insurers who still quote a 14 day child benefit and have legacy contracts within their clientele that have not updated their definition over time. Among all the conversations and feedback we have received through the petition, the overwhelming majority of stakeholders agree that there isn’t a situation that exists where a plan sponsor legitimately “needs” a “from 14 days” definition and these options should simply not exist anymore. The overall opinion from corporate representatives and consultants we spoke with assumed that any plan sponsor with the legacy 14 day child definition likely didn’t realize they even had this definition, and would be mortified if they had to deliver the news to a grieving mother or father that their baby just didn’t live long enough to qualify for a benefit payout. We even heard feedback from a few insurers that they not only had already removed the 14 day benefit from their available option shelf, but had launched even more enhanced options that covered stillbirth after a specified gestation period.

In honour of Patrick and Nolan’s lives and legacy, I, along with 10,042 industry stakeholders, ask CLHIA to support this very worthy initiative in creating a new industry guideline per the below:

Guideline for a New Industry Minimum Standard Child Definition:

Set “from live birth” as the industry minimum standard child definition under group Dependent Life contracts.

Suggested Implementation:

o Any new group benefits quotes for Dependent Life must include this minimum standard definition starting in 2025.

o Any existing legacy contracts with anything worse than live birth (i.e. 24 hours, 14 days, or other) must be amended to the new minimum standard “from live birth” definition by the end of 2025.

Based on my stakeholder discussions and petition with over 10,000 signatures, this issue is an area of common interest within the industry and aligns with CLHIA’s mission. I would be happy to assist in providing any further information or helping in any way that I can do support this initiative.