An explanation of the issue:

As small employers grow in number of staff, they become eligible for increases to the Non-Evidence Maximum (NEM) levels for Life and LTD coverage. An NEM is the amount of coverage an insurer will offer without any medical questions (evidence) being asked for. As an example, a small group with 5 staff might have a $1,500 LTD NEM. If an employee earned $36,000/year, or $3,000 a month, they might be eligible for an LTD benefit that would pay a $2,000 monthly benefit (in the event of total disability). In this example, the first $1,500 of benefit would be provided with no questions asked. The next $500 worth (to get to the $2,000 total) would require to the employee to respond to number of medical questions, and if approved, the employee would then move to the $2,000 level of coverage.

The problem begins when the employee is declined the excess ($500 of coverage) and held at $1,500.

Now let’s assume that the group grows through the year from 5 to 10 staff, and is now eligible (due to that growth) for an increase in the NEM to $2,500. The advisor requests the NEM increase, and it is implemented at the renewal. This means that the next employee hired (at the same earnings) would be provided the $2,000 benefit with no questions asked (as under the $2,500 limit).

The problem is that many insurers would leave that previously declined employee at the older, lower level of coverage of $1,500. As a result, the employee is disadvantaged based solely on their date of hire. I don’t think that this employee inequality is good for any party.

Benefits Canada has now picked up the story HERE

We have over 80% of in the industry in alignment (with 10% pending change).

I’d call that a win.

Here is the interesting part. Most insurers would actually move the employee to the new NEM, if any of the following situations occurred.

- The group moved to another insurer with a higher NEM. The old insurer could then take the case back (a year later) and would grandfather the coverage and add the employee(s) at the new higher NEM level

- The employee left the company and then was re-hired (after 6+ months). The insurer would then take the re-hired employee(s) back at the new higher NEM level

- The benefit (such as LTD) was dropped and was then reinstated at a later date. The insurer would then accept the employee(s) at the new higher NEM level

In all these scenarios the employee(s) would be moved to the higher NEM. So why not, when the advisor and their client remain loyal to the insurer, are they not in return?

We posed the following question to insurers…

A employer has a group plan in place with life &/or LTD coverage. The employee count increases through the year, and as a result they are entitled to an increase in the NEM level(s). At renewal, the advisor (with client consent), makes a request that the plan be amended to the new higher increased NEM. Do you….

1. Increase any employee(s) to the new NEM that have not already applied for the excess LTD above the NEM?

2. Increase any employee(s) to the new NEM that have not already applied for the excess LTD above the NEM, AND also increase those that are in the process of medical underwriting?

3. Increase any employee(s) to the new NEM that have not already applied for the excess LTD above the NEM, AND also increase those that are in the process of medical underwriting? AND increase those that were previously declined?

4. NOT offer to increase the NEM, if there is anyone that was previously declined?

5. Handle these situations in a different way? If so, please provide details.

The survey responses are as follows…

Alberta Blue Cross - 3 (Alberta Blue Cross, at the advisor/employer’s request, will allow all employees that had previously not applied for, proceeded with, or been declined coverage, to be moved up to the new NEM with no medical underwriting, with the exception of those individuals with 0 coverage, which would be considered on a case by case basis) Camden - 3 (follows their market partners) Canada Life (GWL) - 3 The Chamber Plan - 3 Cooperators - 3 Desjardins - 3 Empire - 3 Encon (SSQ) - 3 (some late app./1- life u/w limitations) Equitable - 3 Fenchurch - 3 Group Health - TBC Humania Assurance - 3 Lloyds - 3 Manitoba Blue Cross - (due 2024) Manulife - 3 Medavie Blue Cross - 3 Pacific Blue Cross - (due 2024) RBC - 3 RWAM - 1 (if an amendment is being processed increasing NEM’s, any employee who was previously declined, closed, or is pending would be held at their current amount of coverage and would not be eligible to increase to the new NEM.) Sask. Blue Cross - - (due 2024) SSQ - 3 Sun - 3 (confirmed for SunAdvantage) Unistar - 3 Wawanesa - 3 If your providers' response is not included, please share their response. Last updated 1/11/2024

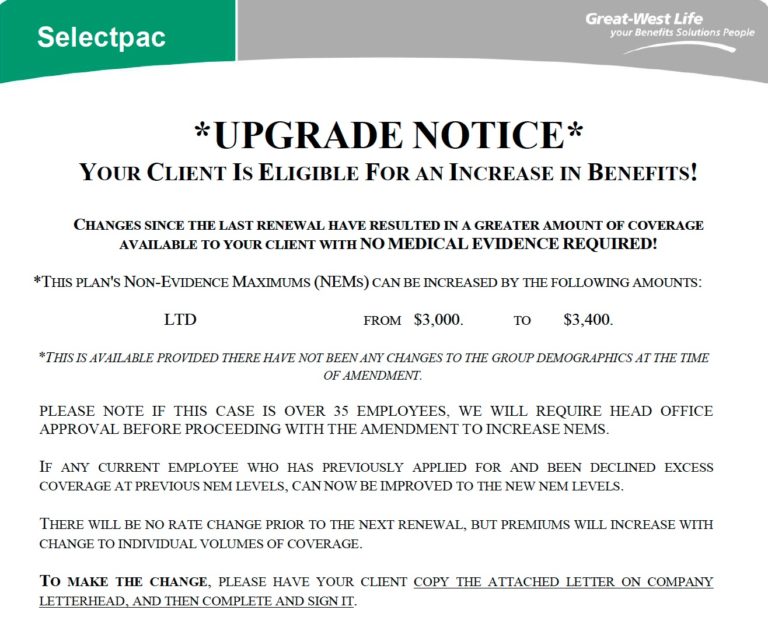

2013 – Great West Life

Great West Life/Canada Life was the industry leader in this area. They began the practice of increasing declined employees (held at an NEM) on their small groups (under 35 lives) to the new, higher NEM as far back as early 2013.

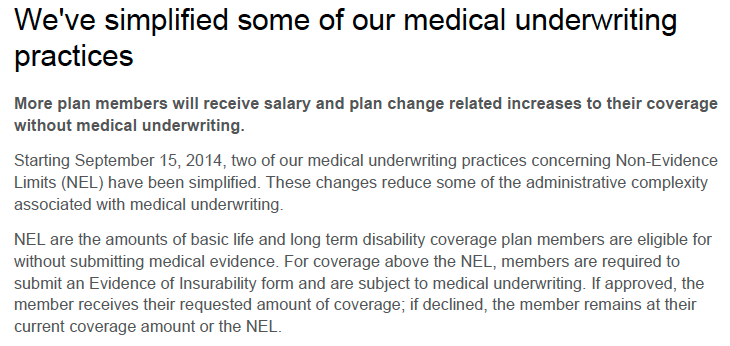

September. 15, 2014 – Manulife

Manulife announces that they were changing and aligning their practice

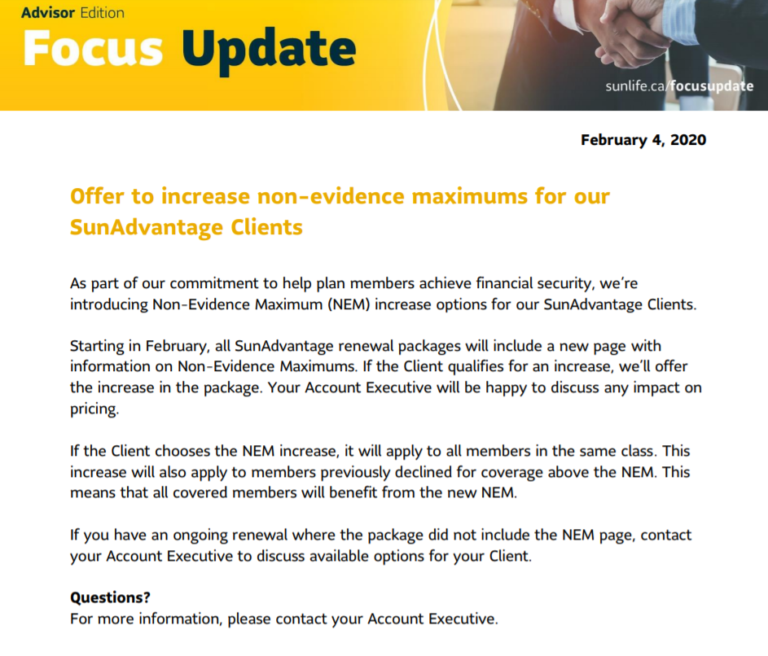

February 4th, 2020 – Sun Life

Sun Life announces that they were changing and aligning their practice

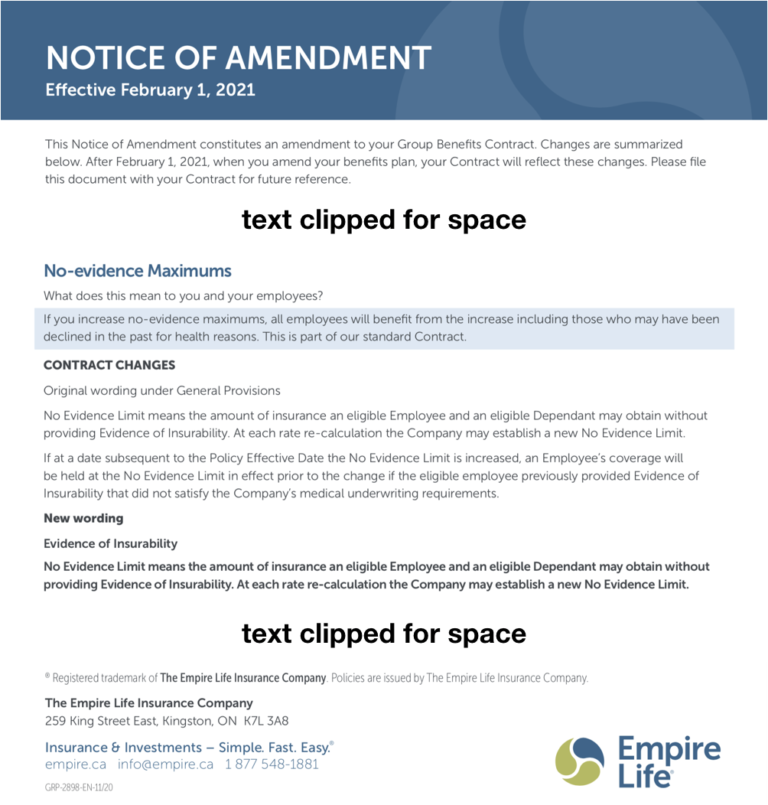

February 28, 2020 – EMPIRE LIFE

Empire Life had announced the change last year but the contract wordings and communications have been going out with renewals. Click on the image below for the full set of amendments.

May 29, 2020 – RBC

Great to see RBC come to the table and put our clients first.

June 18, 2020 – Co-operators

Great to see Co-op add their name and put our clients first.

January 7, 2021 – Benefits by Design (BBD)

Great to see BBD both add their name to the list and communicate it so well to advisors and clients.

“Notice of Policy Amendment

To better protect plan member health, we are updating our Contract and Booklet wording to reflect changes to our Empire Life pooled benefits.

In short, clients with Empire Life pooled benefits will see new wording describing changes to the non-evidence maximum (no-evidence maximum).”

February 3, 2021 – Humania Assurance

This is to confirm with you that Humania does NOT hold back members from the benefit of a higher NEM when the group’s NEM has increased. This applies even if they were previously declined.

Martin Walker – Sales Director, Group Insurance, Western & Central Canada.

February 9, 2021 – Wawanesa Life

Wawanesa confirms that option #3 (as highlighted below), is how we approach the NEM issue. If a Plan Sponsor elects to increase the NEM for the entire group or a class, all eligible employees will have their volumes recalculated up to that new NEM regardless of when they were hired.

3. Increase any employee(s) to the new NEM that have not already applied for the excess LTD above the NEM, AND also increase those that are in the process of medical underwriting? AND increase those that were previously declined?

Dwayne Ashley | Regional Group Manager – Ontario & Atlantic Region

October 31, 2023 – Medavie Blue Cross

As of 2020, it has been our standard practice to automatically increase all members, including those “not applied for” or “declined” when a group’s NEM increases. This increase extends to cases that were underwritten and declined prior to 2020 as well.

Derek Orsini - Medavie Blue Cross

April 4, 2024 – Alberta Blue Cross

Alberta Blue Cross, at the advisor/employer’s request, will allow all employees that had previously not applied for, proceeded with, or been declined coverage, to be moved up to the new NEM with no medical underwriting, with the exception of those individuals with 0 coverage, which would be considered on a case by case basis

Don Forbes - Alberta Blue Cross

Benefits Canada has now picked up the story HERE

We applaud the many insurers for taking the time to respond to the survey and who work with us to ensure both advisors, our clients and their employees are treated fairly and equitably.

Initiatives like this that help bring the industry together rather than creating reasons to be divisive. It kind of makes you wonder what exactly the CLHIA does anyway if not taking this kind of initiative.

We look forward to working together with these insurers on other initiatives in the near future.

This project was an initiative of Dave Patriarche, the founder of CGIB. CGIB is an association dedicated to advisor education and not an advocacy group. The results posted here are for general public reference only and should not be construed as a CGIB initiative, or that it has been supported by CGIB members in any way..